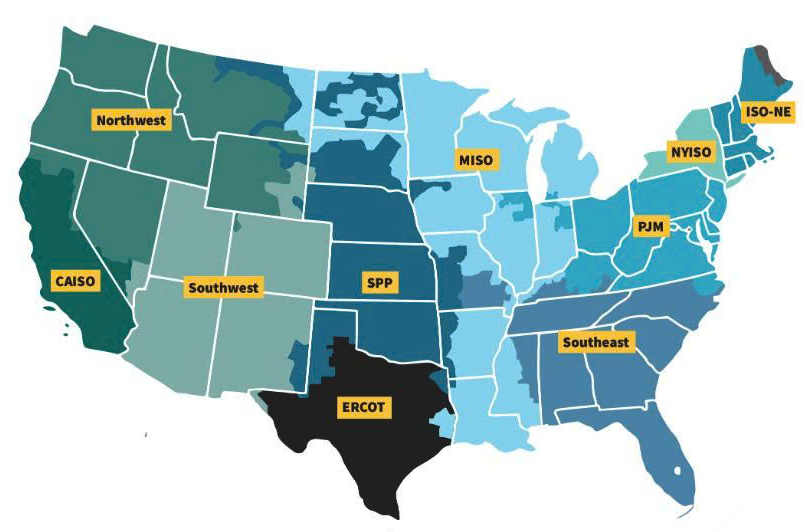

In the United States, there are a total of 7 major organizations that operate as Independent System Operators (ISOs) or Regional Transmission Organizations (RTOs).

The list of these 7 organizations includes:

CAISO: California ISO (California and part of Nevada).

ERCOT: Electric Reliability Council of Texas (Most of Texas – this organization is fully independent and not subject to federal FERC regulation).

ISO New England (ISO-NE): New England region (comprising 6 states: Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, and Vermont).

MISO: Midcontinent Independent System Operator (Midwest and parts of the South).

NYISO: New York ISO (The entire state of New York).

PJM Interconnection: Manages the Mid-Atlantic region (comprising 13 states and the District of Columbia).

SPP: Southwest Power Pool (Central and Southwest states).

Below is a visual overview of the management jurisdictions of these ISOs/RTOs across the United States:

The California Independent System Operator (CAISO) operates a competitive wholesale electricity market and manages the reliability of its transmission grid. CAISO provides open access to the transmission and performs long-term planning. In managing the grid, CAISO centrally dispatches generation and coordinates the movement of wholesale electricity in California and a portion of Nevada. CAISOs markets include energy (day-ahead and real-time), ancillary services, and congestion revenue rights. CAISO also operates an Energy Imbalance Market (EIM), which currently includes CAISO and other balancing authority areas in the western United States.

CAISO was founded in 1998 and became a fully functioning ISO in 2008. The Energy Imbalance Market launched in 2014 with PacifiCorp as the first member or EIM Entity. The EIM serves parts of Arizona, Oregon, Nevada, Washington, California, Utah, Wyoming and Idaho.

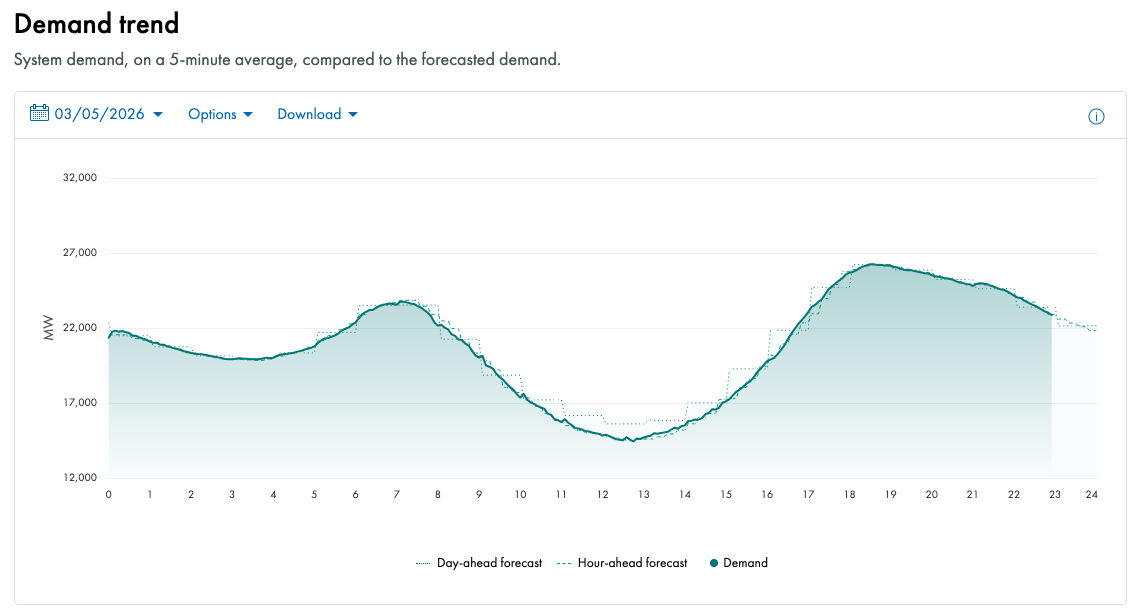

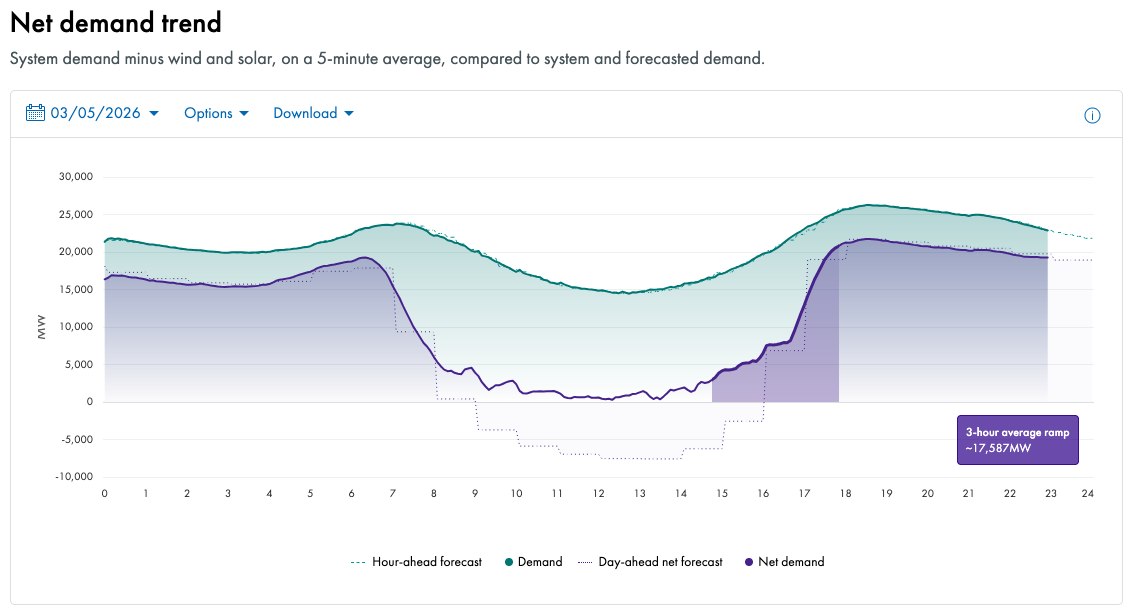

Today's load demand exhibits typical characteristics of a power grid with a high penetration of renewable energy:

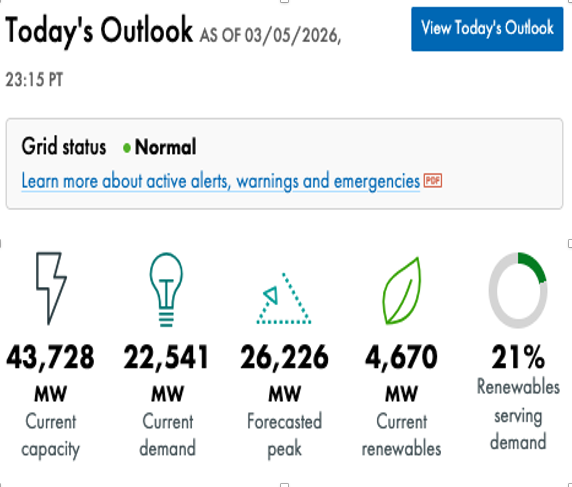

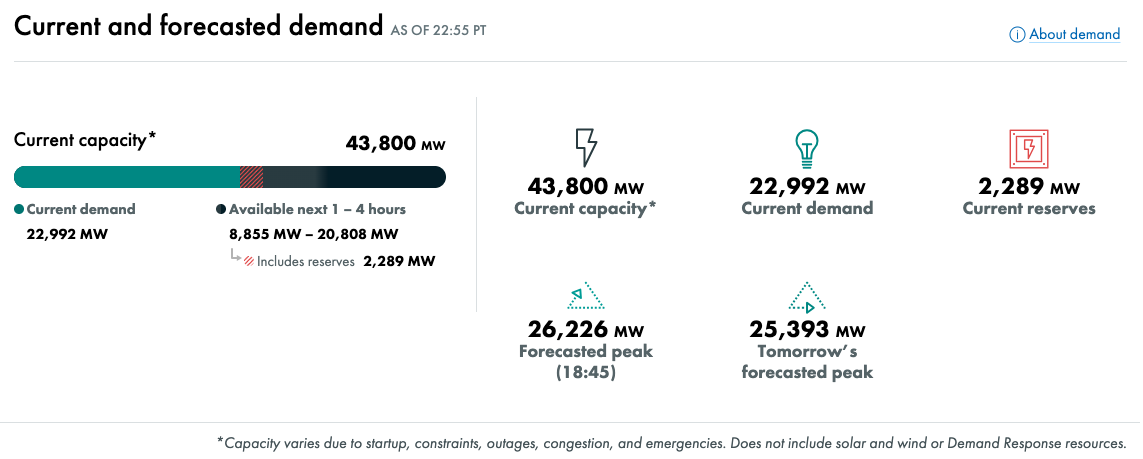

Actual Demand and Forecast: As of 07:05 PT, the actual demand reached 23,759 MW. The forecasted peak demand for the Day-Ahead Market (DAM) is 26,220 MW, expected to occur at 18:30 PT – the period of sunset when residential demand typically surges.

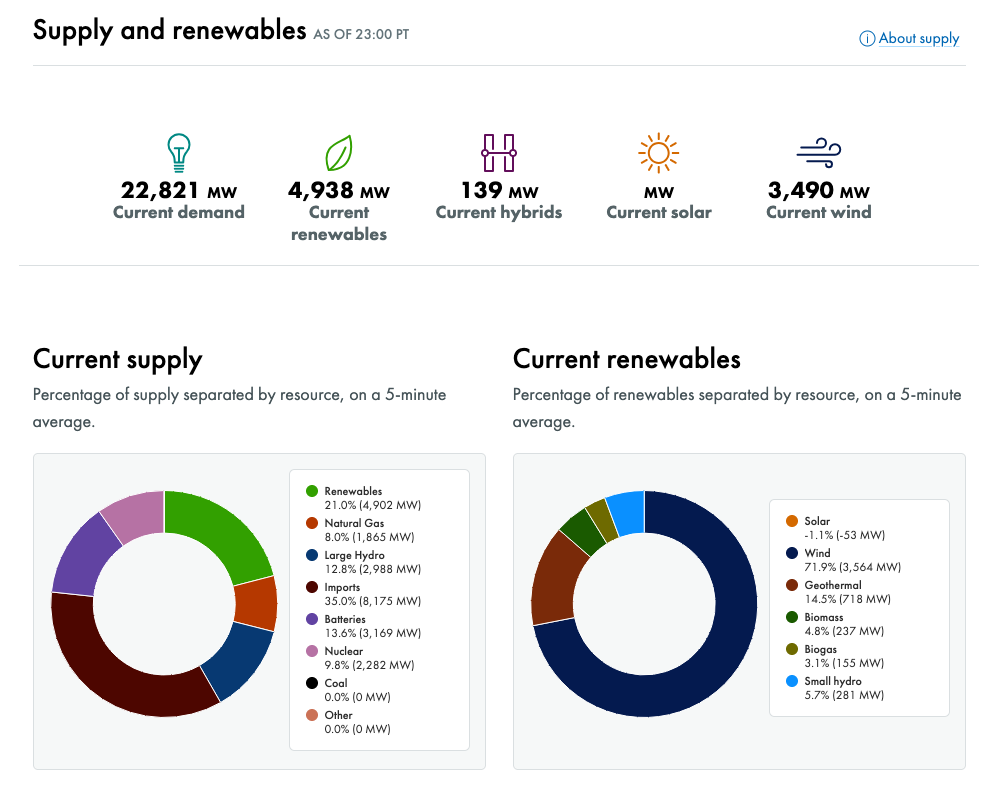

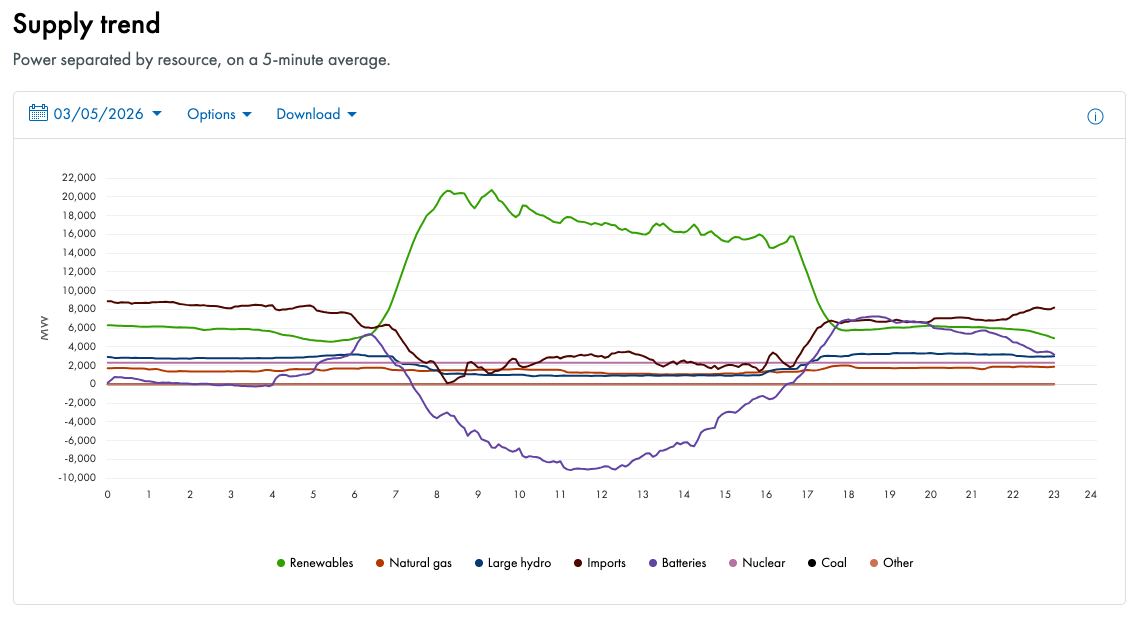

CAISO’s current supply mix is highly diversified, supported by significant contributions from clean energy and imports:

Resource Mix:

Renewables: Account for approximately 21% of the total supply. Within this category, wind power is the primary contributor (approx. 3,500 MW, representing 72% of renewable energy). Solar generation is expected to surge and dominate from 07:00 to 17:00.

Imports: Play a pivotal role, accounting for roughly 35% (approx. 8,100 MW) to maintain system balance.

Large Hydro & Nuclear: Maintain stable contributions at 13% and 10%, respectively.

Natural Gas: Currently deploying about 8% (1,800 MW), with a significant ramp-up expected during the evening peak to compensate for the decline in solar output.

Battery Energy Storage Systems (BESS): Contributing approximately 13.6% to total capacity. The role of battery storage in the DAM is primarily to charge during midday (when prices are low) and discharge during evening peak hours to optimize revenue and support system security.

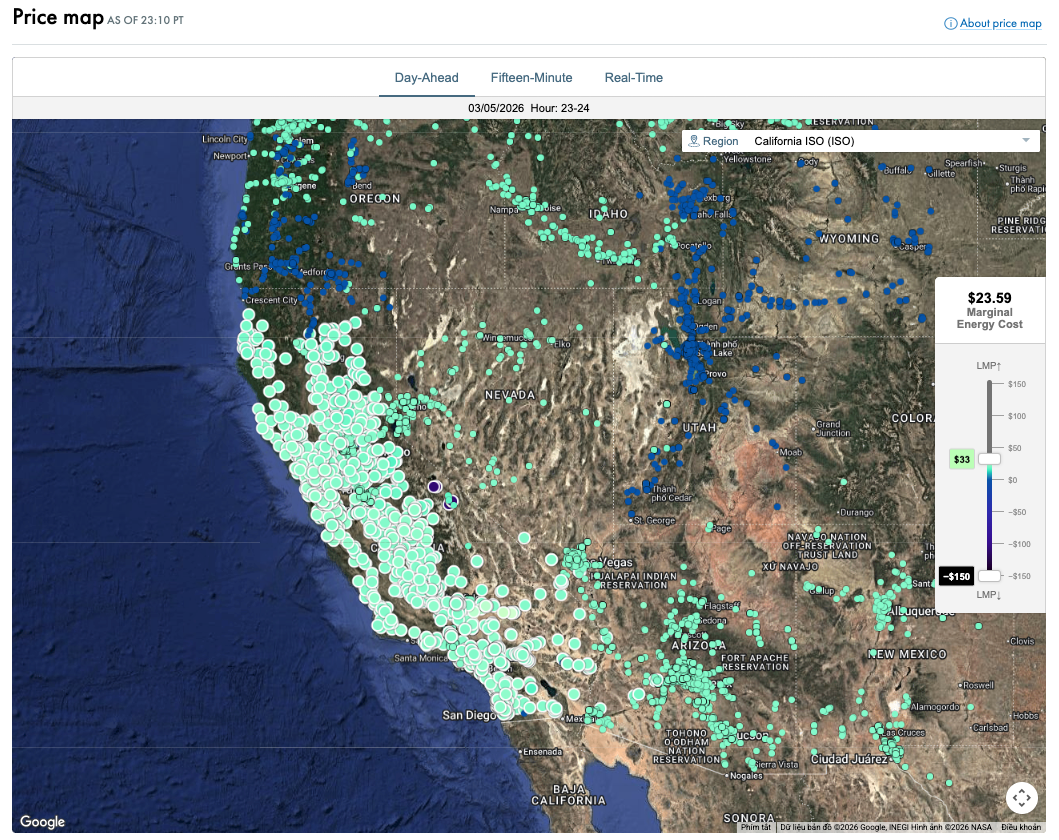

Locational Marginal Pricing (LMP) in the Day-Ahead Market is heavily influenced by fuel costs and the availability of variable energy resources:

LMP Trends: Prices in the DAM are generally more stable than those in the Real-Time Market (RTM). However, there is a distinct divergence between major hubs, such as NP15 (North) and SP15 (South).

Hourly Fluctuations:

Midday: Prices tend to plummet, occasionally reaching negative territory due to solar overgeneration.

Evening Peak: Prices surge due to the combination of peak demand and the solar ramp-down, coupled with an upward trend in natural gas input prices.

Regulatory Mechanism: CAISO applies price mitigation measures to prevent price manipulation in areas affected by transmission congestion.

Source: CAISO

Write a comment

Các trường bắt buộc được đánh dấu *