It is hardly disputable that electricity markets are genuinely political constructs. Policies and regulations shape electricity pricing in order to compensate, incentivize investments, and sustain business cases on both the generation and consumption sides. In the ongoing transition to a low-carbon economy and power sector, retail electricity prices incorporate a plethora of transitionrelated costs – from surcharges financing renewable energy support, to grid expansion, and the costs of balancing, congestion management, and redispatch. Yet, there is a relatively limited understanding of how countries use electricity prices to allocate these costs across consumer groups.

A comparative perspective on retail electricity pricing across consumer groups reveals substantial cross-country differences in the distributional design of electricity pricing regimes. Even within a shared European market and regulatory framework – of which the UK was part until 2021 – the distributional effects of electricity pricing have differed markedly. These differences are not merely technical outcomes but reflect deliberate political choices – choices that are becoming increasingly contested as electricity accounts for a growing share of final energy consumption and expenditures. This article examines how retail electricity prices differ between household and industrial consumers over time and identifies the cost components driving these differences in four European countries: Germany, Spain, Sweden, and the UK. It then considers the policy and regulatory levers shaping price variations across consumer groups, and outlines tentative explanations for the political-economic configurations underlying these choices.

Cross-country variation

Policy and regulatory decisions are often targeted at specific segments of electricity consumers. In most countries, the key distinction is between household and industrial consumers, who differ in consumption patterns and are subject to different regulatory objectives. Consequently, they face different network tariff structures, tax incidence, and exemption or relief schemes. In Europe, the financing of energy transition investments – including renewable energy support and transmission grid expansion – through electricity bills has been the norm, and taxes and levies on retail electricity prices are a central instrument for allocating these costs. As long as costs are recovered within the electricity system, exempting one consumer group inevitably implies higher retail prices for others. Such cross-subsidization raises distributional questions and motivates a closer comparative investigation of cross-country differences.

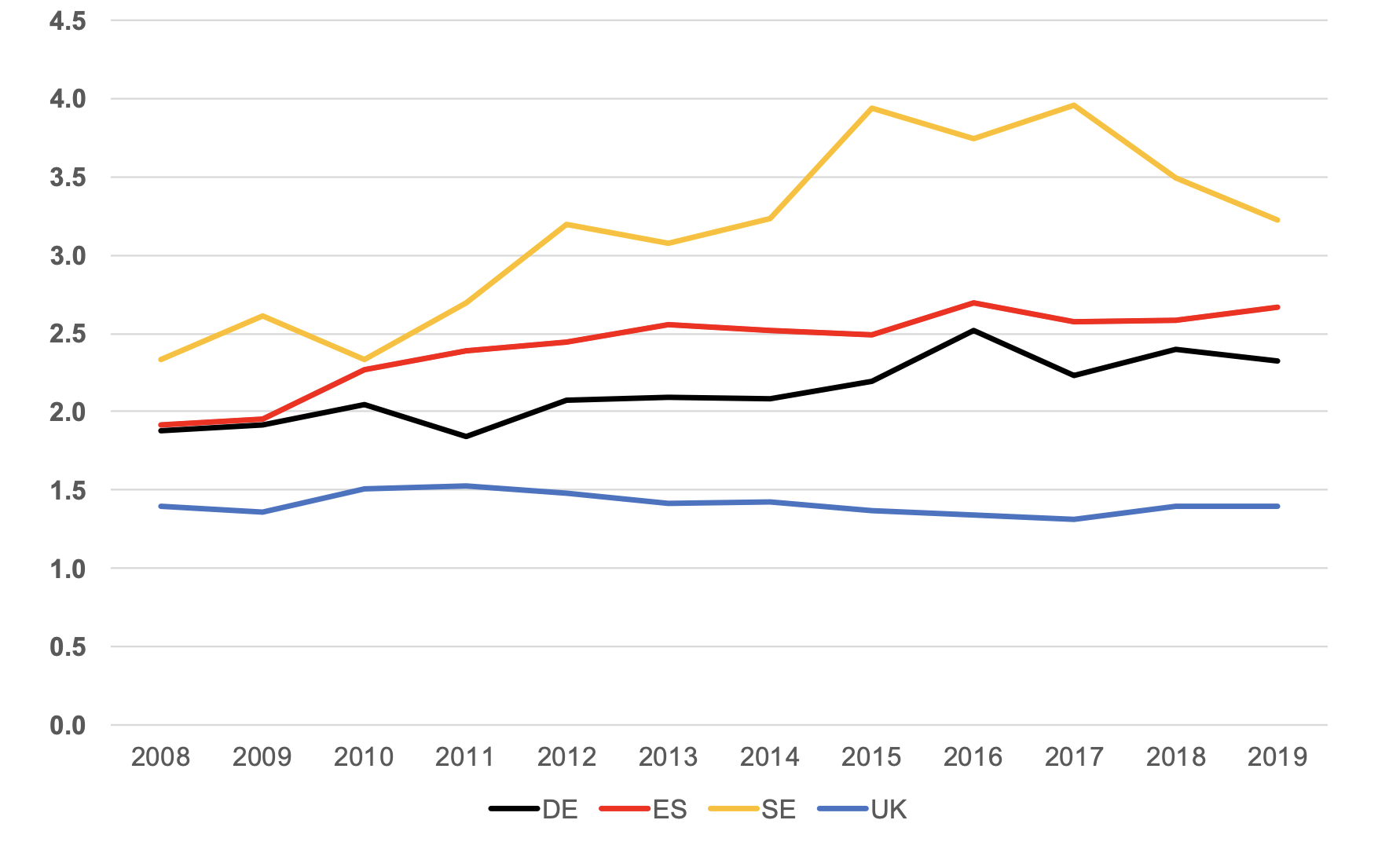

As Figure 1 shows, the household–industry price differential varies substantially across the four countries. In Sweden, households have at times faced almost four times the retail price paid by large industrial consumers, whereas in the UK, household prices are less than 50 per cent higher. In Germany and Spain, households have typically paid around two to two-and-a-half times the industrial electricity price. With the exception of the UK, the household–industry price gap widened over the course of the 2010s.

Notes: Ratio of retail electricity prices of an average household (band DC, 2,500-4,999 kWh/year) and large industrial consumer (band IF, 70,000-149,999 kWh/year). A value of 2.0 means that households are paying twice the electricity price of industry.

Source: Eurostat (2026)

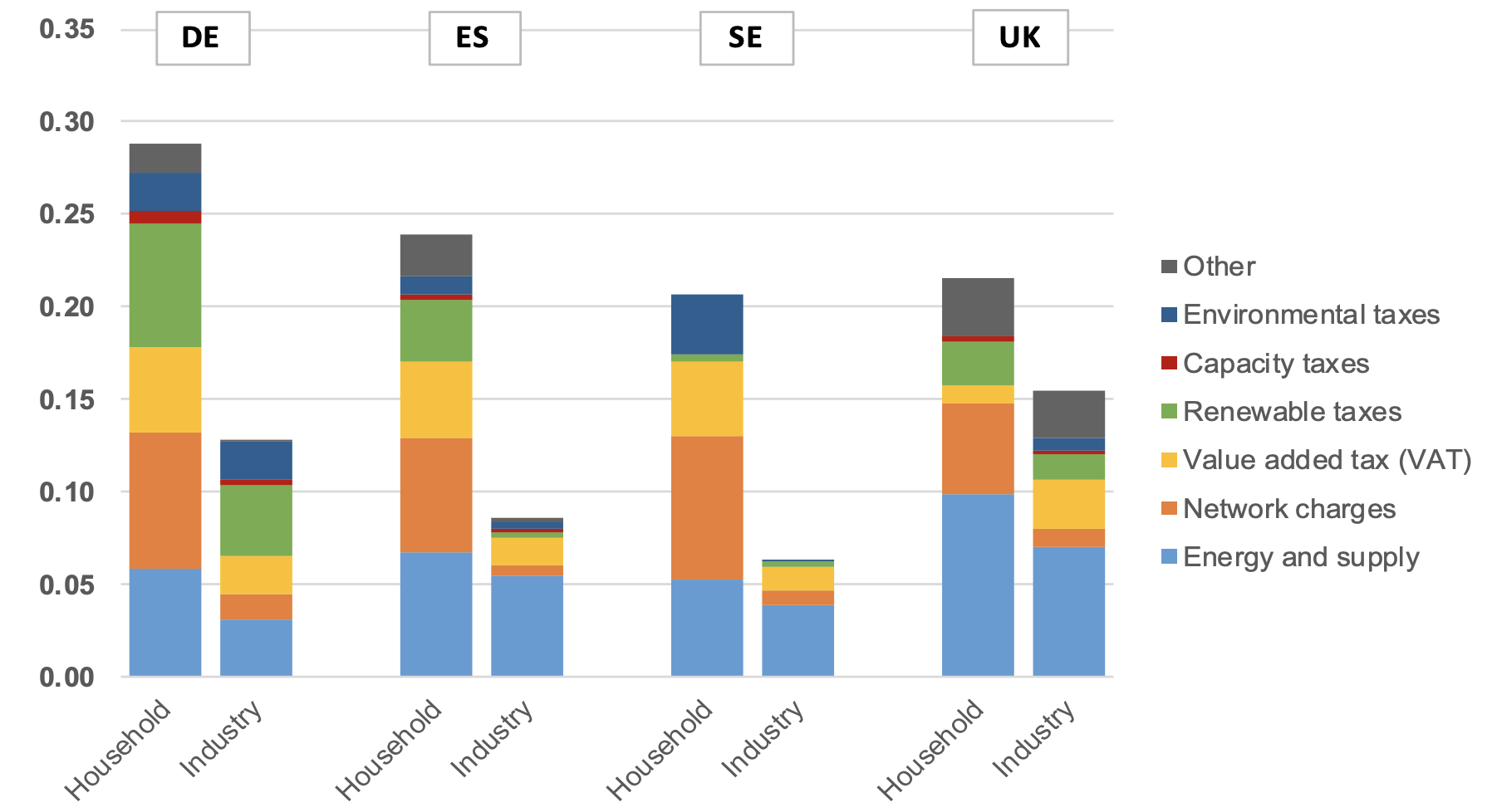

Notes: Electricity price components of retail electricity prices (in EUR/kWh) of an average household (band DC, 2,500-4,999 kWh/year) and large industrial consumer (band IF, 70,000-149,999 kWh/year) for the year 2019. Source: Eurostat

Electricity prices consist of multiple cost components, and differences in these components explain much of the retail price variation between households and industrial consumers (see Figure 2). Across all four countries, network charges, taxes and levies account for most of the household–industry price differential. In the UK, energy costs and network charges are by far the most important drivers, while other taxes and levies partly offset the difference by imposing higher rates on industry than on households. Sweden, by contrast, shifts a larger share of system costs onto households through reduced network charges and lower environmental taxes for industrial consumers. A similar pattern holds in Spain, although renewable energy levies play a more pronounced role. In absolute terms, the largest cross-subsidies are observed in Germany, driven primarily by network charges and renewable energy surcharges. As a result, although energy costs are significantly lower in Germany than in the UK for both household and industrial consumers, household retail prices including taxes and levies are significantly higher in Germany.

As electricity becomes an ever-larger part of the energy mix, these differences have important distributional consequences.

Which policies and regulations drive variation in the price gap between household and industrial consumers? While directly attributing these differences to specific regulations and policies would be an oversimplification, a structured comparison of electricity pricing can help identify patterns in the distributional design of electricity market regulation and policy. To do so, electricity pricing can be compared along three categories, consistent with the Eurostat data used:

The shares of these components vary substantially across countries and consumer groups. For example, the energy and supply component accounts for almost half of the electricity price paid by British households, but only around 20 per cent of the household electricity price in Germany; the remainder is made up of network charges, taxes, and levies. Variation in the household–industry gap within each component is shaped by multiple factors, with policy and regulatory decisions playing a key role.

The cost of energy and supply is shaped primarily by infrastructure and market conditions, including the generation mix and the degree of interconnection with neighbouring markets. Limited interconnection has constrained Spain’s and the UK’s ability to import low-cost electricity. Instead, gas-fired plants have set the wholesale price for more hours of the year than in Germany and Sweden. The household–industry price differential in this component is less directly shaped by policy and regulation, but differences in hedging opportunities and exposure to wholesale prices – partly determined by policy choices such as bidding-zone design – matter. In Germany and the UK, industrial consumers can draw on highly liquid forward markets, whereas households typically pay a premium for long-term fixed-price contracts – contributing to lower energy and supply costs for industry.

Network charges are the single most important contributor to the household–industry price gap across all four cases. In each country, network tariffs decline with higher voltage levels, larger connection capacity, and greater consumption volumes. The household–industry differential in network charges is somewhat larger in Spain and Sweden than in Germany and the UK for two reasons. First, Spanish and Swedish tariff structures recover a greater share of network revenues through non-volumetric charges, which raises unit costs for households in relative terms. Second, Spain and Sweden differentiate tariffs more strongly by voltage level, which results in significantly lower per-unit charges for consumers connected at medium- and high-voltage levels.

At the same time, both Germany and the UK provide explicit exemptions for very large industrial consumers, which are only partly captured in Figure 2. These exemptions are substantially more generous in Germany, where they have implied reductions of 8090 per cent since 2011, whereas UK energy-intensive industries have only since 2024 been eligible for exemptions of up to 60 per cent of network charges.

Taxes and levies drive most of the cross-country variation in the household–industry electricity price differential. Historically, the main source of variation has been the level and allocation of renewable energy support costs. In Germany and Spain, renewable energy support explains around one-fifth of the household–industry price gap, while it plays a much smaller role in Sweden and the UK. Overall, renewable support costs have been considerably higher under the German and Spanish regimes than under the more market-based approaches used in Sweden and the UK. Sweden, in turn, levies substantially higher environmental taxes on households than on industrial consumers. Although Germany has, since 2022, no longer financed renewable energy support through surcharges on electricity prices, increases in other taxes and levies have more than offset the intended reduction in retail prices.

Taken together, two cross-country patterns in the distributional effects of electricity policy and regulation stand out. First, network charges, taxes, and levies generate a markedly smaller household–industry price gap in the UK than in the other three cases. Second, price differentials in Germany and Spain have been more strongly shaped by the costs of expansive renewable energy support than in Sweden and the UK.

Drawing on insights from Comparative Political Economy scholarship – which has so far paid limited attention to energy markets – can contribute to a better understanding of the broader distributional dynamics at play. Given their cross-cutting nature, the allocation of transition costs embedded in electricity prices is likely to be shaped by political dynamics similar to those governing fiscal and other areas of regulatory policymaking.

Recent political economy research highlights how institutions like electoral systems, patterns of interest intermediation, bureaucratic structures, and welfare-state arrangements shape the distribution of policy costs. Consistent with this framework, the UK’s institutional setting offers limited scope to shift costs from industry to households. Its majoritarian electoral system and relatively weak welfare state heighten policymakers’ sensitivity to consumer backlash, discouraging attempts to pass costs onto households. At the same time, pluralist interest intermediation constrains governments’ ability to compensate powerful actors.

A static institutional perspective takes us only so far. To account for the more nuanced differences in distributional patterns across Germany, Spain, and Sweden, it is more instructive to consider how the sectoral structure of each economy’s growth model has shaped energy transition policymaking.

Germany illustrates how industrial-policy objectives and distributional conflict coincide. The high level of renewable energy policy costs reflects the preferences of a large manufacturing sector for an industrial-policy approach to renewable energy support aimed at fostering the emergence of a new technology sector. At the same time, German industry has vigorously defended exemptions from these policy costs, which helps explain why households paid almost twice the renewable energy surcharge paid by industry in 2019 (see Figure 2).

The Spanish case points to the political legacy of the tariff deficit accumulated under the pre-2014 feed-in tariff regime. The deficit emerged in part because policymakers had committed to keeping household electricity bills stable in a context where public acceptance of renewable energy support was politically salient, and where household consumption was a central driver of economic growth prior to the global financial crisis. After the crisis, as Spain became more export-oriented and concerns about industrial competitiveness intensified, policymakers increasingly sought to shield electricity-intensive firms from bearing a proportional share of these accumulated costs.

In Sweden, by contrast, the household–industry price differential has been much less shaped by renewable energy support, reflecting the market-based certificate scheme and its strong emphasis on cost efficiency. Instead, it largely results from exemptions from most other taxes and levies on retail electricity prices, consistent with a long-standing tradition of preferential energy taxation aimed at supporting the competitiveness of energy-intensive industries. These industries continue to shape electricity pricing decisions, particularly as industrial electrification increases the economic and political stakes.

A Comparative Political Economy approach is not primarily concerned with explaining price levels. Rather, it helps identify the political choices underpinning cross-country variation in the distribution of electricity costs, and the macro-institutional settings in which these choices are embedded. Building on this perspective, a research agenda that develops more detailed empirical accounts can provide a context-sensitive understanding of how distributional conflict shapes electricity pricing, informing policies that promote more equitable market arrangements and stronger political support for the energy transition.

Source: Link

Write a comment

Các trường bắt buộc được đánh dấu *