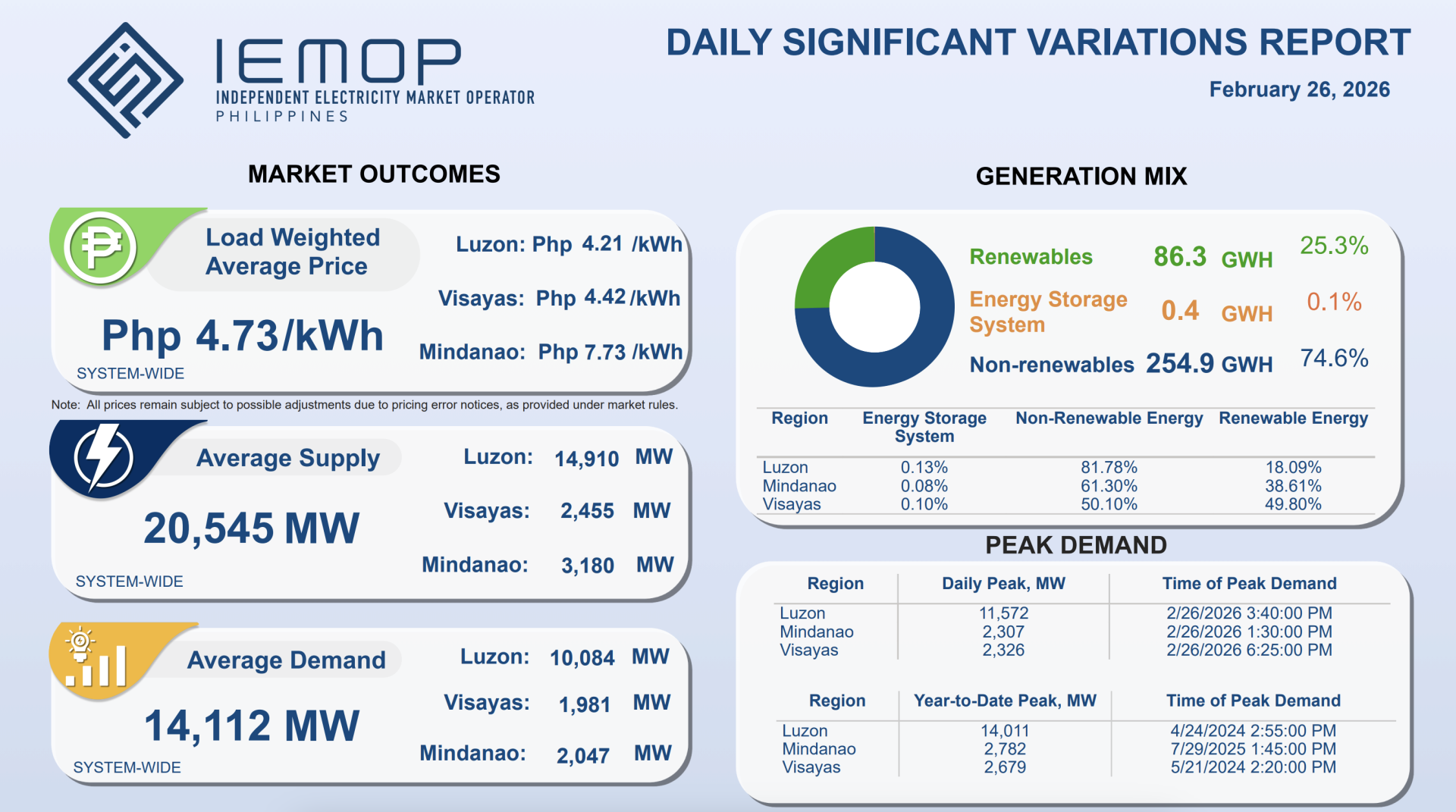

1. Market Overview (Market Outcomes)

Load Weighted Average Price

- System-wide: 4.73 Php/kWh

- Luzon: 4.21 Php/kWh

- Visayas: 4.42 Php/kWh

- Mindanao: 7.73 Php/kWh

➤ Analysis

- Mindanao records the highest price, nearly double that of Luzon, possibly due to:

+ Transmission constraints

+ Higher-cost generation (thermal/diesel)

+ Localized supply–demand tightness

- Luzon has the lowest price, reflecting a larger generation portfolio and stronger market competition.

Supply and Demand

- Average Supply: 20,545 MW

- Average Demand: 14,112 MW

➤ Observations

- The system reserve margin is relatively large (~6,400 MW).

- There are no signs of system-wide power shortage.

- However, high prices in Mindanao indicate localized imbalance rather than a nationwide shortage.

2. Generation Mix

Total daily generation:

- Non-renewables: 254.9 GWh (74.6%)

- Renewables: 86.3 GWh (25.3%)

- Energy Storage: 0.4 GWh (0.1%)

➤ Analysis

- The Philippine power system still relies heavily on thermal generation (~75%)

- The renewable share (~25%) is moderate.

- Energy storage systems (ESS) currently play a negligible role.

Theo vùng:

| Region | Non-Renewable Resouces | Renewable Resouces |

| Luzon | 81.78% | 18.09% |

| Mindanao | 61.30% | 38.61% |

| Visayas | 50.10% | 49.80% |

➤ Notable points:

- Visayas has nearly 50% renewable penetration, indicating strong energy transition progress.

- Mindanao has a relatively high renewable share (~39%) but also high prices, possibly due to transmission constraints or renewable intermittency.

- Luzon remains more dependent on thermal generation.

3. Peak Demand

Daily Peak

| Region | MW |

| Luzon | 11,572 |

| Mindanao | 2,307 |

| Visayas | 2,326 |

→ Peak demand occurred between approximately 13:00 and 18:25

Year-to-Date Peak

| Region | MW |

| Luzon | 14,011 |

| Mindanao | 2,782 |

| Visayas | 2,679 |

➤ Analysis

- Current demand has not yet reached the annual peak.

- The system retains operational headroom.

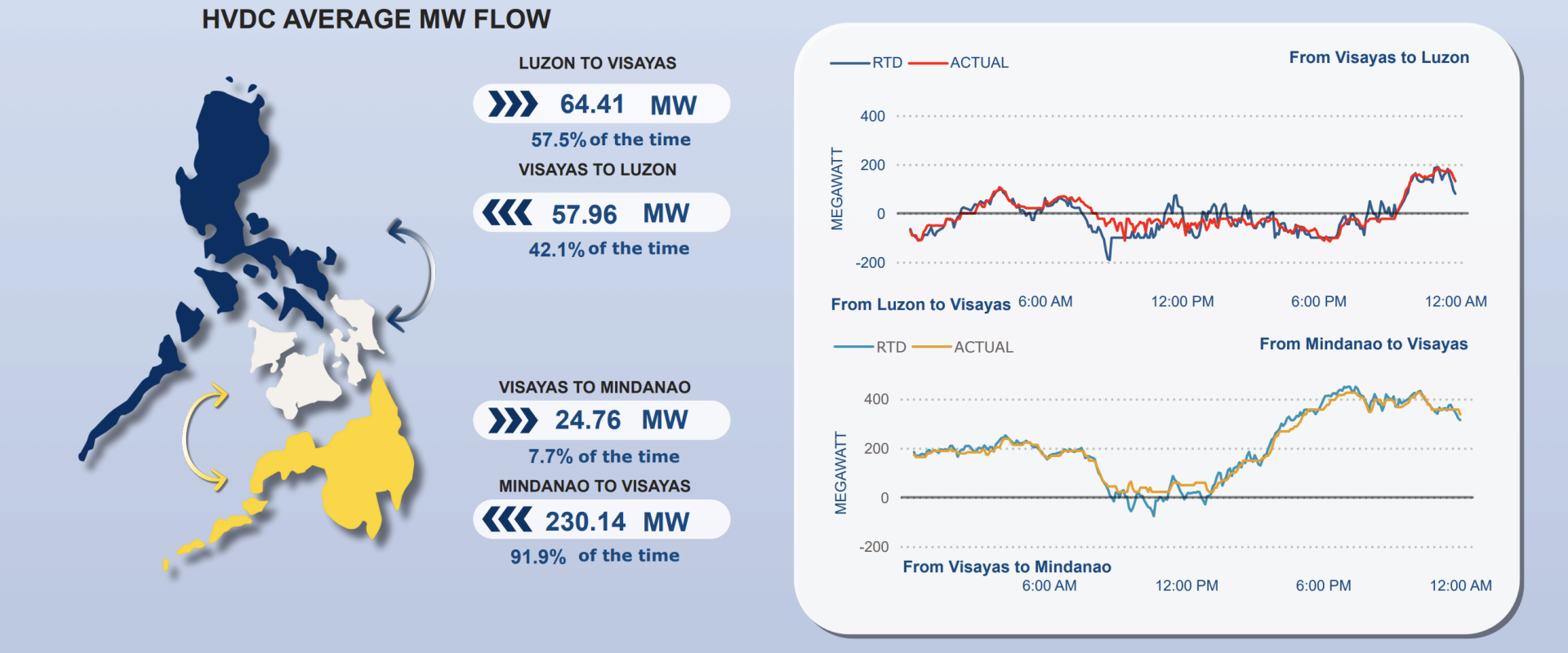

4. HVDC Power Flows (Interconnection)

- Luzon ↔ Visayas

+ Luzon → Visayas: 64.41 MW (57.5% of the time)

+ Visayas → Luzon: 57.96 MW (42.1% of the time)

- Visayas ↔ Mindanao

+ Visayas → Mindanao: 24.76 MW

+ Mindanao → Visayas: 230.14 MW (91.9% of the time)

➤ Key insights

- Mindanao exports electricity to Visayas most of the time.

- However, Mindanao still experiences higher prices, possibly because:

+ Exports reduce available local supply

+ Zonal pricing separates regional markets

+ Internal transmission constraints exist

- The Philippine system operates as a multi-island grid, heavily dependent on HVDC interconnections.

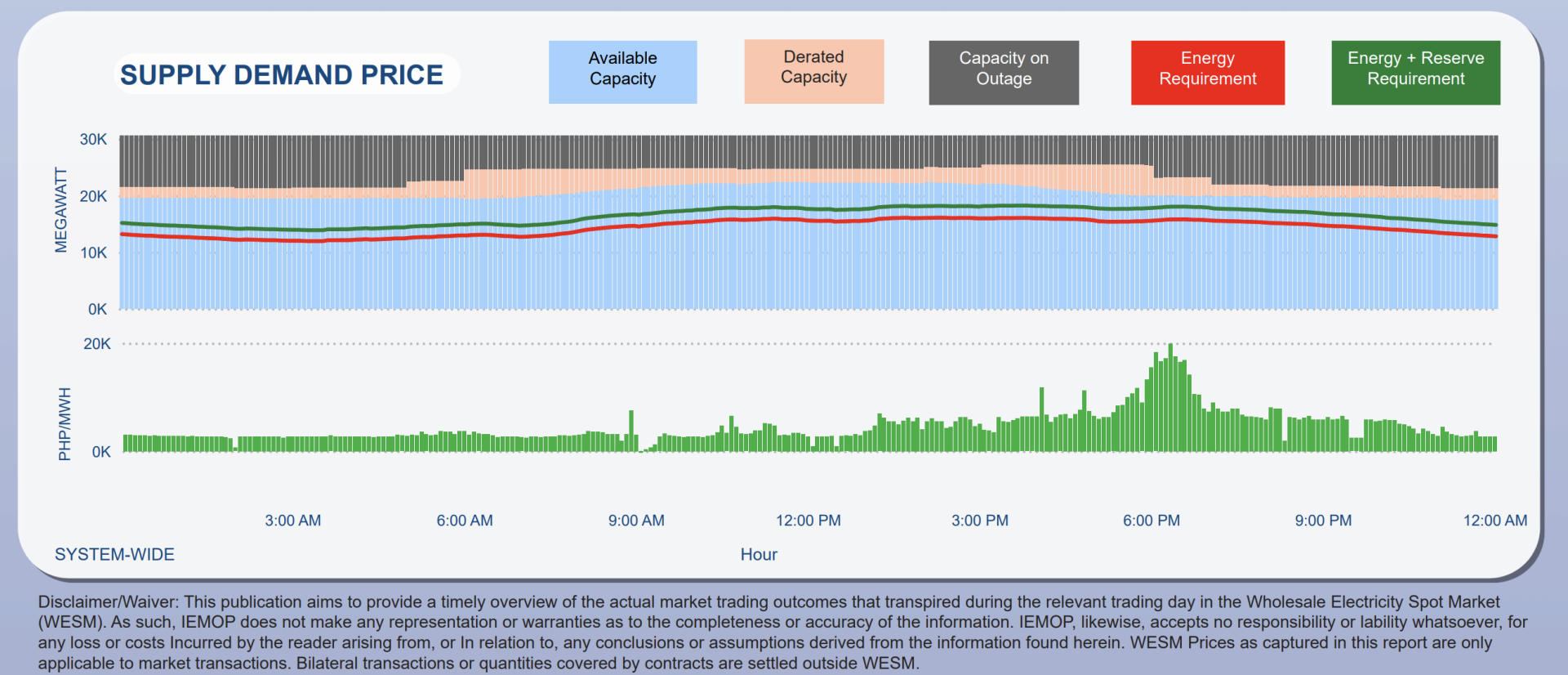

5. Supply – Demand – Price Chart

Observations:

- Capacity available cao hơn energy requirement

- A noticeable price spike appears around 18:00.

- In the early evening, demand increases while renewable output declines (solar sunset effect).

➤ This resembles the “duck curve” phenomenon:

- Lower prices during the day

- Higher prices in the evening

6. In-depth Assessment (Electricity Market Perspective)

Market Structure

- Philippines operates under:

+ Wholesale Electricity Spot Market (WESM)

+ Zonal pricing

+ Market-based dispatch

Key issues:

1. Price differentials across islands

2. Transmission constraints influencing prices

3. Increasing renewable penetration but insufficient ESS deployment

4. The critical role of interregional coordination mechanisms

7. Overall Conclusion

- There is no nationwide electricity shortage.

- Localized imbalances exist.

- The system remains heavily dependent on thermal generation.

- Renewables are increasing but lack sufficient flexibility support.

- Prices are volatile in the early evening.

- Inter-island transmission plays a decisive role in market outcomes.

Source: IEMOP

Write a comment

Các trường bắt buộc được đánh dấu *